TECH-OVER: AN OVERVIEW OF MERGERS AND ACQUISITIONS IN DIGITAL MARKETS

by Elena Salomone

Companies active in digital markets are remarkably involved in mergers and acquisitions (“M&A”), constantly seeking out interesting start-ups and purchasing them.

One common concern raised by these transactions is that they may have the objective of preventing the target company from ever becoming a competitive threat. This may be especially problematic in the context of digital markets, where, due to network effects, often competition is for the market rather than in the market and where, the competitive threat exerted by small market players or potential entrants is essential to discipline incumbents’ market behavior. Another reason for concern is that most of this M&A activity occurs beyond the radar of competition authorities as the vast majority of these transactions generally do not meet the thresholds that trigger merger control. Indeed, merger control thresholds are often based on the merging parties’ turnover, which are rarely met when targets are start-ups that in some instances are still trying to figure out a viable path to monetization.

For the aforementioned reasons, it is interesting to analyze the characteristics of the M&A activity carried out by digital incumbents to understand whether they reveal any reason for concern. In the context of the ex-post assessment of merger control decisions in digital markets carried out on behalf of the UK Competition and Markets Authority (available at https://www.learlab.com/publication/ex-post-assessment-of-merger-control-decisions-in-digital-markets/), Lear looked at the M&A activity carried out by Amazon, Facebook and Google in the period between 2008 and 2018. Over this period, based on the publicly available information collected, Google has acquired 168 companies, Facebook 71 companies and Amazon 60 companies.

The objective of this analysis was understanding the main characteristics of the target companies and, in particular, what type of economic activity they performed and their age at the time of the transaction.

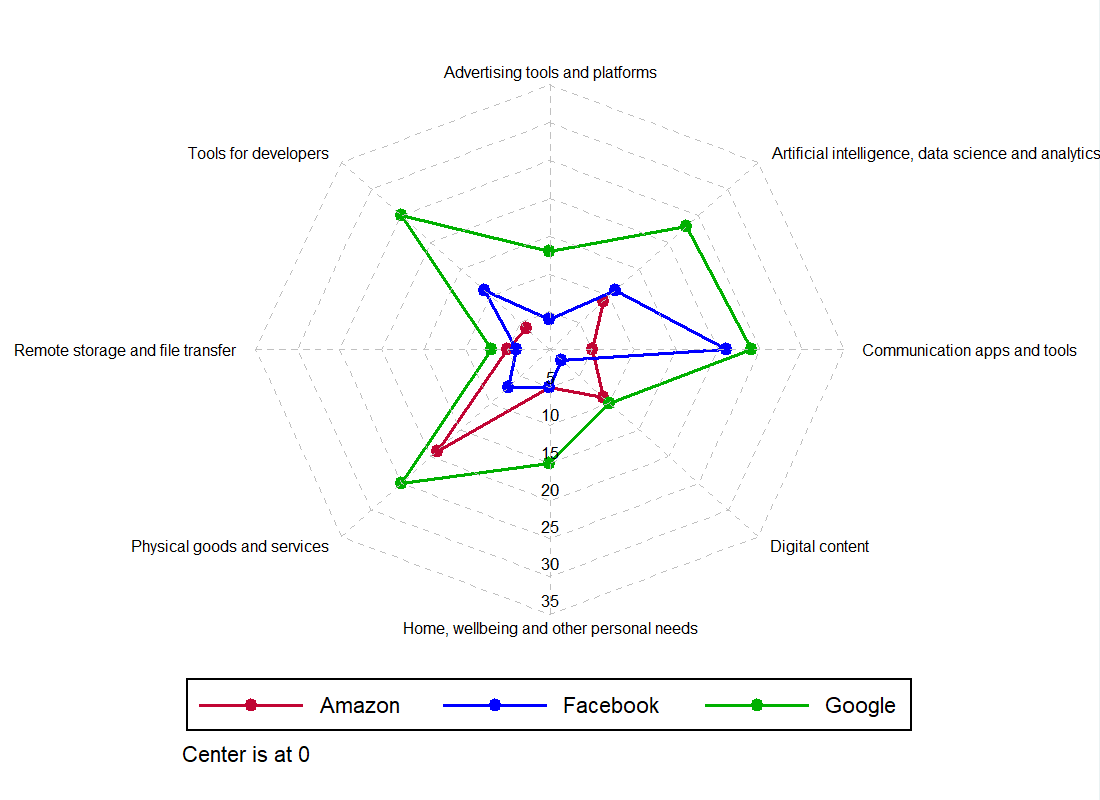

Target companies were grouped in clusters depending on their sector of economic activity. In terms of absolute volumes, Google has been remarkably more active than Amazon and Facebook, having bought out more companies than the other two in each of the clusters, as shown by the figure above. The picture also reveals that Google’s acquisitions have been more heterogenous in nature, whereas:

Amazon and Facebook seem to have focused more on companies that were active in the same area of economic activity, respectively: Physical goods and services and Communication apps and tools.

Some common trends can be identified in the M&A activity of these three companies. All of Amazon, Facebook and Google, indeed, have:

- propelled their push into mobile also through the acquisition of companies that have helped with the development of services optimized for use from mobile devices;

- invested into companies that have helped them with advanced data analytics techniques (machine learning, artificial intelligence, analytics and big data). These companies heavily rely on making predictions of various sorts to provide their services. For instance, Amazon uses them to manage its stock based on expected demand; Facebook to propose targeted content and ads to its users; Google to improve its search algorithms and target ads more accurately. Hence, these mergers may be efficiency-enhancing as they enable incumbents to become better at making such predictions.

Another striking feature of the acquisitions carried out by Amazon, Facebook and Google is that their targets are often very young firms. While there are some outliers, targets are four-year-old or younger in nearly 60% of cases. The median age of the targets, however, is slightly different across the three companies: 6.5 for Amazon; 2.5 for Facebook; and 4 for Google.

The competition policy implications of this analysis are the following:

- the volume of transactions is significant; this implies that these companies have an acquisition strategy that is not taken into consideration in merger control where the assessment is constrained to the competitive effects of the single transaction;

- targets are typically very young firms; at that stage in their life cycle their evolution is still uncertain and it is difficult to identify the relevant counterfactual against which the effects of the merger should be assessed; this may call for a lower standard of proof in the application of the SLC test;

- though with notable exceptions, most transactions would seem to have a non-horizontal nature; target companies are active in a wide range of economic sectors and their products and services are often complementary to those supplied by Amazon, Facebook and Google; on the surface, this finding could be reassuring, as the concern that digital incumbents’ M&A activity has the main objective of preventing targets from becoming a competitive threat seems less likely; in addition, non-horizontal mergers present significant scope for efficiencies; however, this finding also highlights the complexity of the business models pursued by digital companies, as several activities seem to enter into their productive process and the limitations of an assessment based on narrowly defined markets; moreover incumbents of digital markets may prevent actual or potential rivals from obtaining the efficiencies that may be realized through these acquisitions.

News & Events

News & Events

26 March 2024

PAOLO SPEAKS AT THE ITALIAN ANTITRUST ASSOCIATION

19 March 2024

Lear is looking for a Junior Consultant

13 March 2024

Market study for DG Comp on online payment services

Read all news >

Sign up

Sign up for updates on our publications, events and seminars.